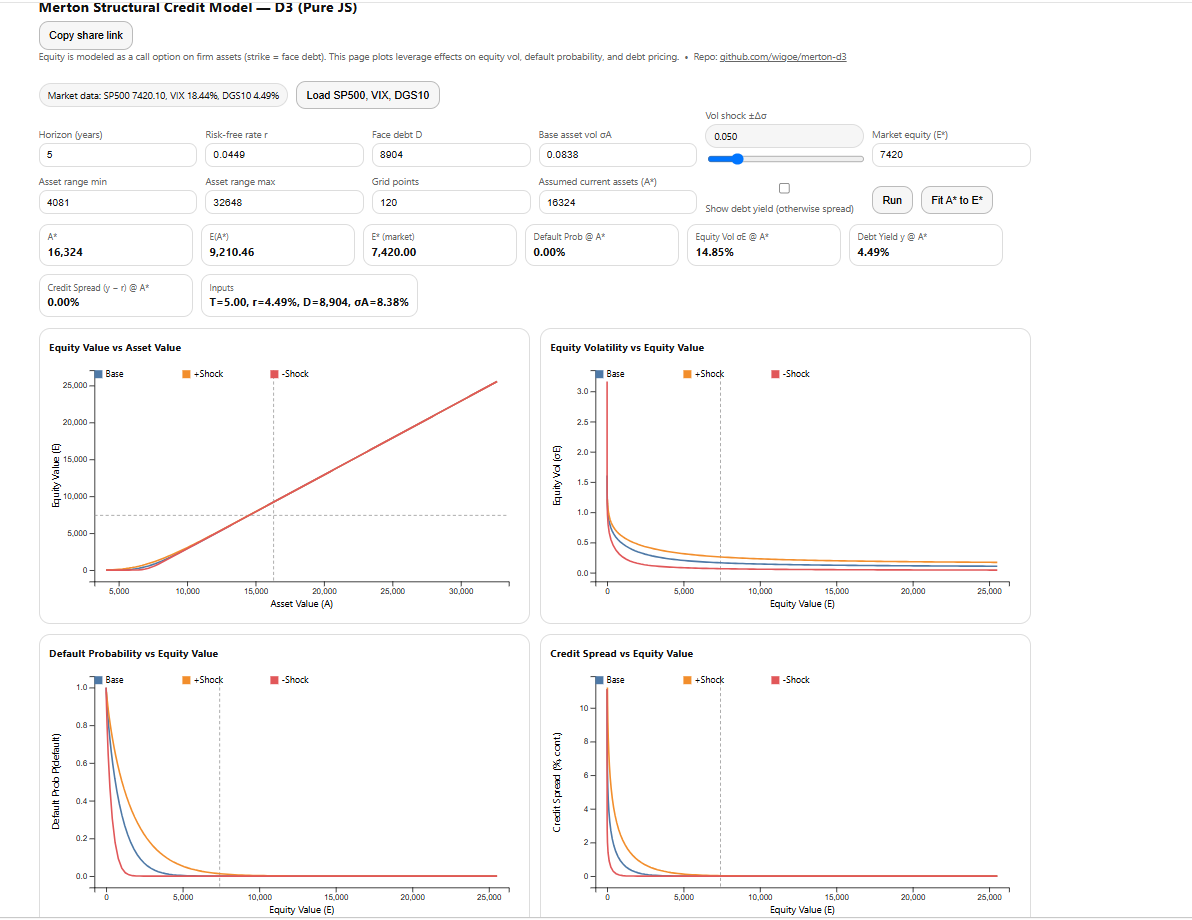

Explore the interactive Merton Model

The recent rally in the S&P 500 and the steady decline in corporate credit spreads prompted me to revisit the Merton Structural Credit Model.

Developed by economist Robert Merton, the model treats a firm's equity as a call option on its assets. By combining equity values, debt levels, interest rates, and volatility, the framework provides a useful way to think about default risk and corporate credit spreads.

After fully repairing and updating my implementation of the model, I calibrated it using current market data from RainbowStats. The results suggest that corporate credit remains relatively healthy. Equity values are sufficiently above the implied default boundary that a substantial market decline would likely be required before credit quality begins to deteriorate meaningfully.

The model highlights an important concept: credit quality is often less sensitive to modest market fluctuations than many investors assume. When asset values remain comfortably above outstanding debt obligations, credit spreads can remain compressed even during periods of market volatility.

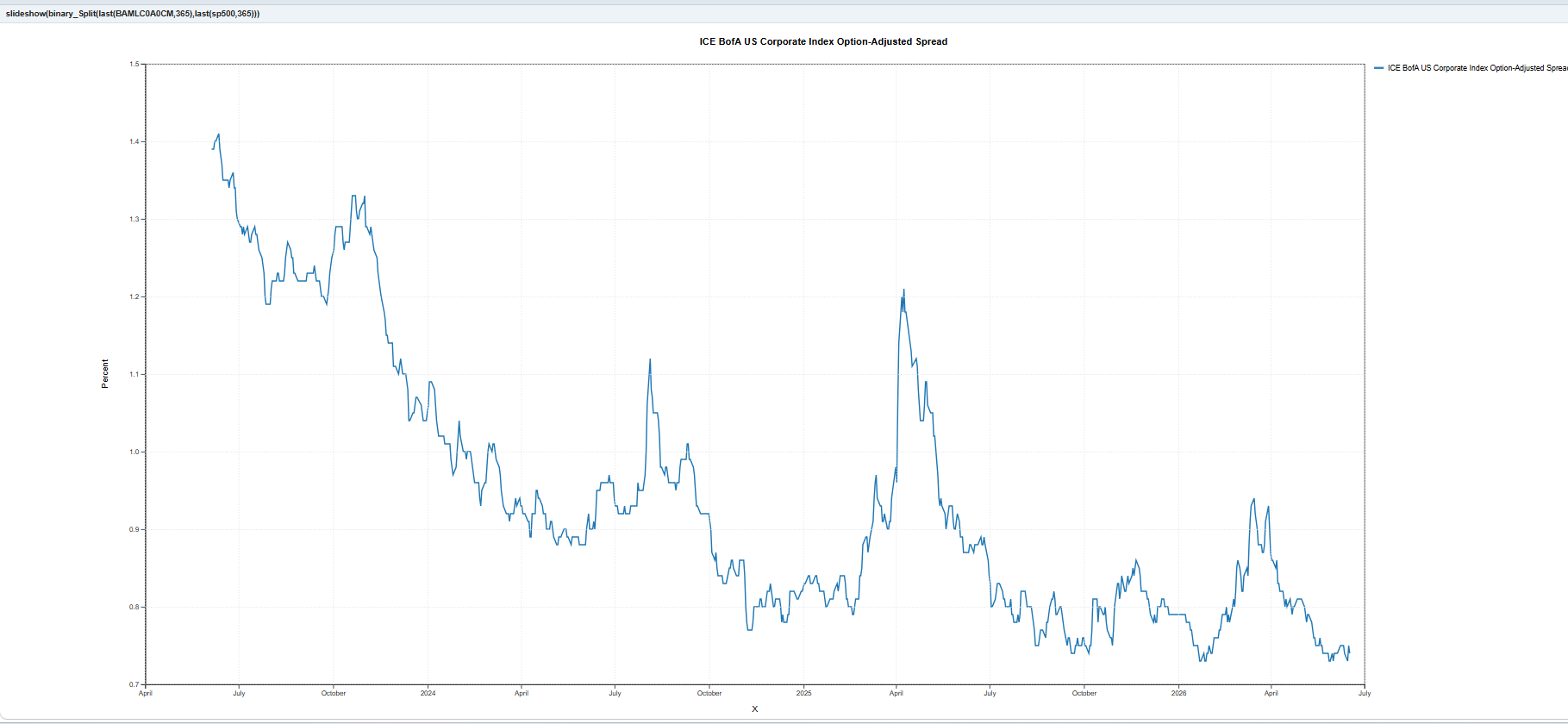

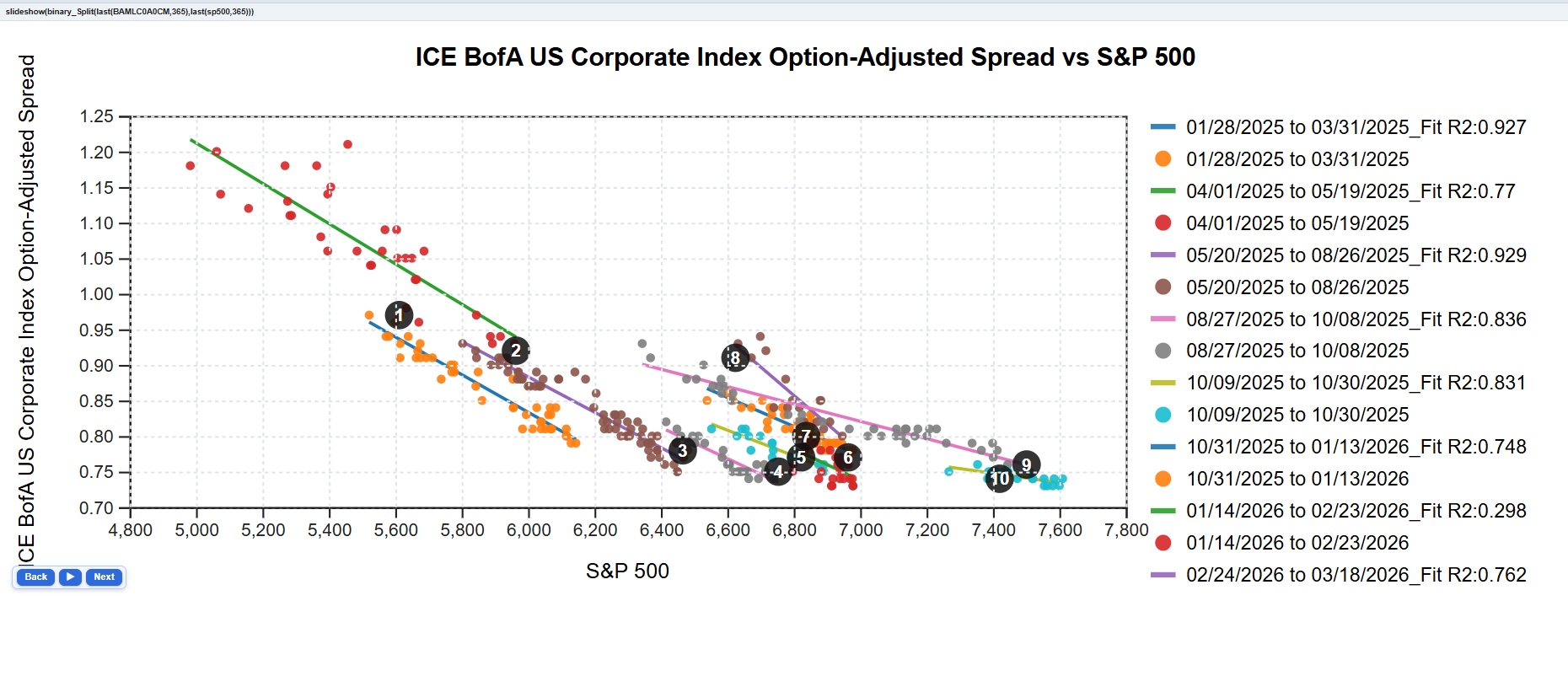

To further explore the relationship between credit spreads and equity prices, I applied the RainbowStats Binary Split analysis to corporate credit spreads and the S&P 500.

The first chart below shows the historical relationship between the ICE BofA U.S. Corporate Index Option-Adjusted Spread and the S&P 500.

The inverse relationship is evident: as equity markets rise, corporate credit spreads generally narrow. During periods of market stress, spreads widen as investors demand additional compensation for credit risk.

The Binary Split analysis reveals distinct market regimes and highlights how the spread-equity relationship changes across different market environments.

Explore the interactive Binary Split analysis

Together, the Merton model and Binary Split analysis tell a consistent story. Equity markets remain elevated, corporate balance sheets appear resilient, and credit spreads continue to reflect relatively benign default expectations. While conditions can change quickly, current market pricing suggests that it would take a significant deterioration in equity values before credit risk becomes a major concern.

RainbowStats continues to evolve as a platform for combining financial modeling, econometrics, and interactive visualization. Projects like these help bridge the gap between financial theory and practical market analysis.